THE RETAIL MANAGER

THE RETAIL MANAGER

is MMC2's first Mobile Computing Crystal released for general use.

Actually The Retail Manager is a double crystal combined in one:

- double as in it combines the power and functionality of two crystals.

- double (1) to introduce the power of mobile computing crystals to the market, and (2) to celebrate the beginning of a new era, and a new, simple, easy way in business computing.

The FIRST CRYSTAL is a powerful, yet simple to use, MONEY COUNTING TOOL, designed to count and balance cash register and point of sale (POS) tills, and other money floats.

YOU CAN TAKE THE CRYSTAL TO THE TILL.

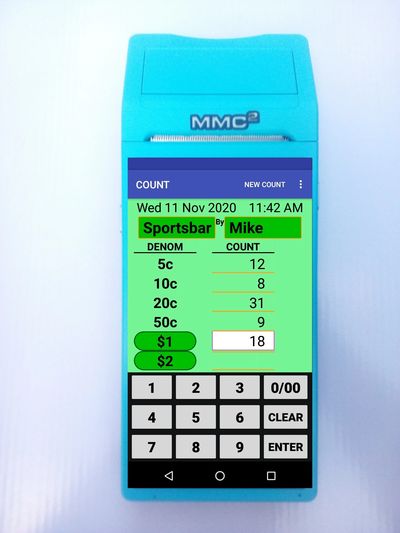

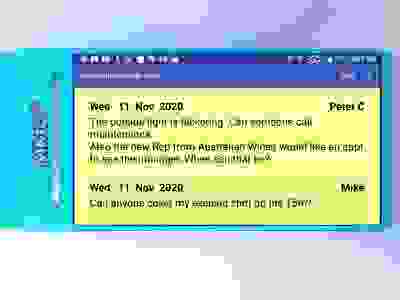

First Crystal - MONEY COUNT showing '18' being entered as the counted number of $1 coins.

The SECOND CRYSTAL is a collection of USEFUL TOOLS for the retail manager. It provides convenient and well organised electronic versions of the following:

- Business Mission Statement

- Statement of current and previous management focus issues

- Staff communications book

- Store Notice

- Store opening procedure

- Store closing procedure

- Phone numbers with notes

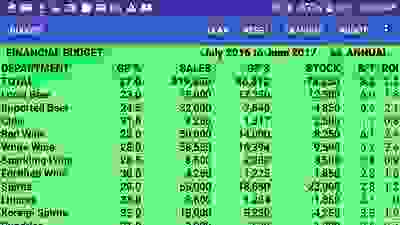

Second Crystal - showing the actual menu, listing the functions including the Budget Planning Tool

And the

- Sales, Stock, and Profit, Budget Planning Tool. This in its own right, is worthy of the status of being a mobile computing crystal

What can

THE RETAIL MANAGER, (the MOBILE COMPUTING CRYSTAL)

do for

the retail manager, (the person)?

The many answers to this question, can be summarised by referring to the following self assessment certificate. If you would like to be able to legitimately claim the competencies and standards of practice listed, then the MMC2 RETAIL MANAGER will be very useful to you and your business. The first six standards of practice are underpinned by the ease, speed, accuracy and presentation of money counts, when performed by the Money Count feature. The seventh standard of practice concerns the advantages to staff, and hence to the business, of keeping electronic versions of the most often required, store paper records and notices. These advantages include the professional presentation, including neatness and legibility, as well as availability, including all in one central location, and also the ease of use and of updating of them. The remaining seven items involve organising stock into departments and making use of the Sales Stock and Profit Budget Planning Tool. Only too often, the preparation of budgets is left to the accountant, and regarded as a necessary but not entirely welcome task. And once completed, they are looked at once or twice, and then left to gather dust. The Budget Planning Tool changes all of that. MMC2 have successfully condensed the essence of planning budgets, into App form, and have made tinkering with the budgets much more available and attractive. This in turn results in their more frequent use, which in turn makes it much more likely, that serious financial modelling and budget planning, becomes more highly rated in the retail manager's mind. Budgets become living documents, and useful and used tools. The final two items - Stockturn Rate and Return on Investment, are two essential Retail statistics, that are generated automatically by the Budget Planning Tool, and the retail manager is encouraged to explore these concepts more, and to make use of the insights that these statistics can reveal. Using the MMC2 Retail Manager Crystal, to qualify a retailer in accordance with this certificate, can help to transition a shopkeeper into becoming a retail manager.

The SALES, STOCK and PROFIT

BUDGET PLANNING TOOL

AND NOW IN MORE DETAIL

THE FIRST MMC2 CRYSTAL - MONEY COUNTING TOOL

Retail business managers usually invest a lot of time and effort into controlling stock. They can spend significant sums on stock control, including computerised stock control systems, stocktakes, both internal as well as external, store layouts and shelving etc.. But they don't always go to the same extent to control money. Selling stock for money is the purpose of having costly inventories of stock. It follows, that careful professional control of money, is at least as necessary as state of the art stock control methods. This is one reason why retailers have cash registers, which provide essential ways of controlling money. But events and possibilities between sales being rung on the cash register, and the money being deposited in the bank, can sometimes be partly neglected. The money in the till has to be counted, and reconciled with cash register totals prior to it being entered into the store's accounting system, and being banked. But cash register till's should be counted for more than this basic purpose. Best practice requires the till to be also counted at the beginning of the day's trading. Otherwise it is assumed that the beginning float is correct. We all know what assumptions can make of you and me. And there will inevitably come a time when the beginning float is not correct. This adds an unnecessary degree of difficulty to balancing the till at the end of trading. Best practice also sees several till counts throughout the day to isolate any discrepancies, and to reduce the size of the task of tracking down the causes of such. Till counts should certainly be done at change of shift, and where different sales staff start using the cash register. Random spot till counts are a useful method for the retail manager to take proactive steps where it is suspected that sales staff may not be ringing all sales correctly, especially where there is the intention of taking out the cash equivalent of under rung sales later, but prior to balancing at the end of the shift. Another reason for a till count is in the situation where a customer claims that they paid with a higher denomination note than the sales staff believes. A quick till count can often resolve this situation. The issue here revolves around 'quick'. If there is not a lot of money to count and not a queue of waiting customers, then the count is relatively easy. But it is not always so, and this can place pressure on the staff doing the count. Pressure when counting money is usually counterproductive to both speed and accuracy. This observation about pressure when counting money, is also applicable to all of the above reasons for counting cash register tills.

It is generally accepted, that in busy retail stores, there will frequently be small discrepancies between the cash register totals and the money counted. There is usually some margin for error accepted, and after all, what can you do about these discrepancies without considerable costly time and effort. But even regular, small discrepancies can mask significant shrinkage from the retail store's net profit. A daily shortage in one till of $2.50, over a 365 day trading year amounts to over $900. Yet at $2.50 per day it is barely noticeable.

Fast, easy, accurate and efficient money counts, provide best practice to control such shrinkage. The Retail Manager money counting tool is one way of achieving such counts. Some cash registers and POS terminals have money counting features that fulfill this function. But many retail stores get by using calculators and handwritten bits of paper for this important task. This method often requires more than one attempt, particularly when the first attempt of the count does not agree with the cash register total. When this happens the question becomes 'Is it a discrepancy or did I make an error in the count.' The Retail Manager money counting tool takes the count entered for each denomination and extends it by the value of the denomination to give the total value for that denomination. Then it automatically calculates the total for all denominations, to give total cash. It has the name of each cash register and its float value stored. This allows it to automatically subtract the float from total cash to give cash to be banked.

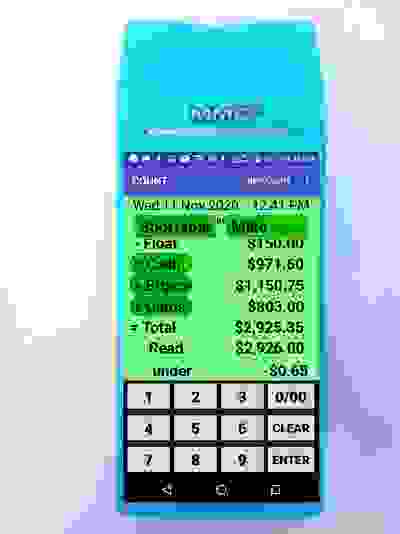

MONEY COUNT scrolled down showing the Total. Cash, Eftpos and Cards can be balanced individually.

There is an option to automatically allocate the number counted for each denomination, into how many for float and how many to be banked. This feature is useful in notifying the staff preparing the banking, as to how many of each denomination to take and how many to leave. In practice it might tell the staff to take the small number of coins in each coin denomination, to leave a small number of notes for the smaller note denominations, and to take the rest for the larger note denominations. The staff can be confident that the 'to be banked' amount will be correct, as will the float left for the next day's trading. The Money Count also handles EFTPOS and Credit Card reconciliations. It also provides for Cheques where required and miscellaneous vouchers.

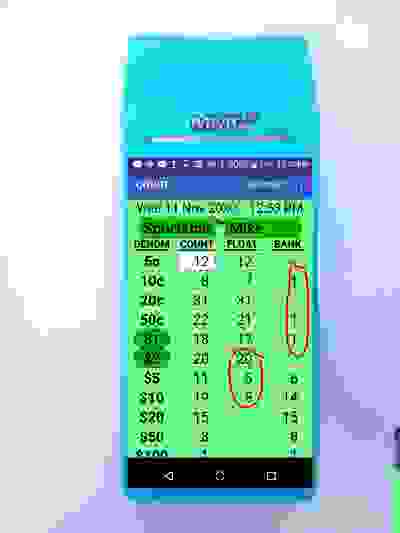

With FLOAT automatically calculated. Take the top marked counts and leave the lower marked counts.

The Retail Manager Money Counting tool issues a machine printed summary of the reconciliation, including the name of the cash register being counted, the staff member's name, the date and time of the count, the denomination counts, details of EFTPOS, Credit Cards etc, totals and discrepancies. Another helpful use of the money count is where cash register tills are counted and balanced at each cash register, and then the money for banking is taken to the store office, where it is recounted and the takings prepared for banking. Recounting, although repetitive, is necessary to ensure accuracy and honesty. But where the count has been performed using the Retail Manager Money Counting tool, and a copy of the printed summary is provided to the office, along with the takings, the office only needs to count the number for each denomination provided on the summary, to ensure that the takings declared have actually been handed over. If the individual denomination counts agree with the printed summary, and they should, because the till has already been balanced with discrepancies noted at the cash register, then the extended values and totals that have already been done and printed on the summary will be correct. This makes the office function of counting, much easier and quicker. Regular as well as unscheduled till counts allow the retail store management to be proactive in establishing and maintaining tight money controls.

Money counts can be saved and stored electronically in the file. This provides an easy and convenient way to review earlier counts in the day, or counts from previous days, that may be queried. There is a recount facility that can be useful in cases where a count was interrupted for some reason. Instead of recounting or re- entering the numbers, simply save the count, and then recall it and continue when convenient. There is also a fine adjustment feature. This is useful where staff may have completed the count just prior to closing, and a customer comes in right on closing. Let's say the customer tenders a $20 note, and receives $7.50 change. The fine adjustment feature allows the staff member to add '1' to the $20s and to subtract '1' from the $5, $2 and 50 cents denomination counts. This is quicker and less open to error than re-entering the new counts for the affected denominations.

Place holder for printed summaries.

THE SECOND MMC2 CRYSTAL - COLLECTION OF USEFUL TOOLS

The second crystal is a collection of useful tools for the retail store manager. The value of these items lies in their convenience, organisation and the ready availability of the information stored within them. All of these records are stored electronically, in one central place and easily updated. Gone are bits of paper and sticky tape, and dog eared exercise books that can easily be misplaced amongst piles of paper.

- Business Mission Statement

Best practice is not content for the retail manager to assume that they already know the purpose of the business and that they have no need to write it down. Sometimes the business mission might need to incorporate new opportunities. Some avenues can contract or even close down, and some change direction. For example the licensee of a small hotel might think " I run a pub - that is my mission full stop". But reflection on the business mission statement, might provide the opportunity to consider opening up and promoting the accommodation side of the business, instead of relying on bar sales only. Perhaps becoming affiliated with a local sporting club might become part of the mission statement. The benefits of having an up to date and well written business mission statement that is readily available for review and for updating, as a method for keeping the management team focused, cannot be over stated. Refer to any business best practice source.

- Statement of current and previous management focus issues

A storekeeper opens the doors each morning and trusts that the customers will come in and that profitable sales will be made. A retail manager always has at least one or two specific matters that are under review and where improvement is sought. A written statement of these issues is of great help in keeping them in mind and maintaining focus on them. A written history of these issues, together with notes on useful methods employed, and problems faced, becomes a handbook for the successful management of the business.

- Staff communications book

- Store Notices

- Store opening procedure

- Store closing procedure

- Phone numbers with notes

The above five items provide the advantages of having well organised electronic, legible, easily updateable, readily available and professionally presented versions of written records commonly used in retail stores. The additional advantage is having them all together and stored on a medium that is not likely to be easily mislaid.

Showing an excerpt from the scrollable STAFF COMMUNICATIONS BOOK.

And last but by no means least, in the second mobile computing crystal, is the Sales, Stock, and Profit, Budget Planning Tool.

What is the prime objective of a retail business, or in fact any business? The answer has to be profit. Profit is a good and necessary thing. Without it a business cannot survive long term. If the business cannot survive, then any other objectives become merely academic, as they cannot possibly be achieved. Profit does not imply grossly unfair rip offs imposed on unsuspecting and vulnerable victims. Governments are in place to ensure fairness and ethical behavior. In the words of the Skyhooks song "Ego is not a dirty word", also "Profit is not a dirty word". Profit can range from achieving break-even, to being rewarding for initiative and effort, and to being lucrative. It is the role of the retail manager to plan for and manage PROFIT.

How does the retail business earn profit? Answer - by purchasing and selling stock. The retail manager has to plan and manage how to achieve the sales that will deliver the planned profit. It is the management function to research and plan for what stock will sell and at what price. Then management has to plan for the stock that will be required to be financed, purchased, and maintained, that will allow these sales to take place. So it is the role of the retail manager to plan for and manage SALES and STOCK.

There are obviously many other matters that require the retail manager's expertise, and time and attention, such as staff, premises, statutory requirements, advertising and promotion etc etc, But THE RETAIL MANAGER Sales, Stock, and Profit, Budget Planning Tool provides a very easy to use tool to assist with planning, ie budgeting, the three fundamental tasks of the retail manager ie planning and budgeting for Sales, Stock, and Profit. This is done by financial modelling, which is surprisingly easy on this crystal. It is easy to use, but very relevant to the heart of the retail management function. To use it, the manager speculates about and enters proposed profit amounts that might be achieved. The tool then reflects what sales would be required to achieve this profit. Dollar profits depend on sales and gross profit %s. So the manager can try a series of 'what ifs' around changing sales targets and profit margins. And all of this is done not only on total sales and profit, but by department. This allows the manager to delve into that area where by a general rule of thumb, 70% of sales comes from 30% of the stock, or some such situation. The manager then considers the effects of reducing some departmental targets and increasing others. At all times the manager takes into account that these are numbers that are meant to indicate what might transfer into achieved results, along with the many other considerations that affect sales and profit percentages. The Budget Planning Tool allows the manager to enter the stock levels, by department, that will be required, in their experience, to serve as the foundation for the sales and profit targets being pursued.

The Budget Planning Tool shows the rate of stockturn, which is an indication of how fast or slow a department and the store overall stock is turning over, similar to a speedometer on a car. Stockturn rates are useful for comparing with previous years and also with expected rates in the industry as well as with similar type stores if available. Stock standing still is not good and should, unless there be other reasons for keeping it, be sold off as quickly as practical with the capital released being invested into more productive stock. The manger is interested in fast stock turnovers as well, in order to unveil the reasons behind them, so that they might be capitalised upon for even better results. The rate of stockturn is an indication of the health of the retailer's range of stock and of stocklevels. It can also be an indicator of the retail manager's skill and judgement in deciding what to order, and how much to order. Best practice in Retail Management would surely include any reasonably available tools that will aid the retail manager in making these decisions and in developing their skills and judgements in making these decisions. Improving knowledge of stockturn rates, both within the business, and with comparable stores, should feature often and prominently on the Management Focus issues list.

ROI - return on investment is automatically calculated for each department and the store in total. ROI shows in financial terms how worthwhile it is keeping the stock in each department considering the profit made and the amount of investment in stock required. ROI also is useful in its own right, as well as for comparisons with previous years and for industry figures that might be available. ROI is a vital indication of the health of a retail business.

BUDGET PLANNING screen. Note the totals line on the top. The screen scrolls allowing 16 departments.